So, you’ve reached a point where your current commercial space just isn’t working anymore, and the end of your lease is nowhere in sight. It’s a tight spot many businesses find themselves in, but getting out of a commercial lease is more common than you might think. It’s not about failure; it’s a strategic business decision.

The first move isn’t to panic or call the movers. It’s to find your lease agreement and sit down for a serious read.

Your First Steps to Ending a Commercial Lease

That thick document you signed, full of dense legal jargon, is now your most important tool. You need to read it—not just skim it, but really dissect it. This agreement lays out all the rules and, believe it or not, often contains the very instructions you need for an early exit.

Don’t let the language put you off. You’re on a mission to find specific clauses that deal with ending the lease before the official end date.

Locating Your Exit Routes

Think of your lease as a roadmap. Right now, you’re looking for the designated off-ramps that the lawyers built into the contract. Certain clauses are designed specifically for situations like this. Zero in on these:

- Break Clause: This is the jackpot. An early termination or ‘break’ clause is your most direct path. It will spell out exactly how and when you can end the lease, including how much notice you need to give and any fees involved.

- Assignment and Subletting Provisions: These clauses are your Plan B. They detail whether you can find another business to take over your lease (assignment) or if you can rent the space out to someone else while you remain the primary tenant (subletting). Almost every time, you’ll need the landlord’s permission.

- Default and Remedies Clause: This part of the lease is less of an exit route and more of a ‘what if’ scenario. It explains what happens if you simply stop paying rent and walk away. Knowing the penalties helps you understand the financial risks involved.

It’s also smart to put yourself in the landlord’s shoes. In the Australian commercial property market, landlords live and die by tenant retention. A stable, long-term tenant means predictable income, so they’re naturally hesitant to see you go. This insight is your starting point for negotiation.

Assessing Your Legal Grounds

After you’ve scoured the lease for your contractual options, it’s time to think about whether the landlord has given you a reason to leave. This isn’t about finding a sneaky loophole; it’s about determining if the landlord has failed to uphold their end of the bargain.

Has the landlord breached a fundamental part of the agreement? Maybe they’ve failed to maintain the building, leaving it unsafe or unusable. If so, document everything. Keep a record of dates, take photos, and save all your emails and letters to the landlord. This evidence is pure gold—it’s your leverage.

A much rarer path is the legal concept of ‘frustration’. This applies when a completely unforeseen event makes it physically impossible to continue the lease, like the building being destroyed in a natural disaster. The legal bar for this is incredibly high, but it’s an option in extreme cases.

This initial deep dive turns a big, stressful problem into a clear, actionable plan. Once you’ve done your homework, you’ll be ready to negotiate. And while you’re planning your departure, our complete office relocation checklist is a great resource to make sure nothing gets missed in the move.

If you feel like you’re the only one in this situation, you’re not. Data on the Australian commercial leasing market shows that for every 100 commercial tenants, about 22 explore ending their leases early. Knowing this can give you the confidence to move forward.

Before you talk to your landlord, get familiar with the key terms in your agreement. The table below breaks down the most critical clauses you should find and understand immediately.

Key Lease Clauses to Review Immediately

| Clause Type | What It Means for You | Action Required |

|---|---|---|

| Early Termination (Break) Clause | This gives you the explicit right to end the lease early, but it will have strict conditions like notice periods and potential penalty fees. | Find this clause and note down the exact dates, notice requirements, and any costs. This is your clearest exit path. |

| Assignment & Subletting | These clauses allow you to transfer your lease to a new tenant (assignment) or rent out the space yourself (subletting). | Check the conditions. You’ll almost certainly need the landlord’s consent, and they may have the right to vet new tenants. |

| Default & Remedies | This outlines the penalties if you breach the lease (e.g., stop paying rent). It details what the landlord can legally do. | Understand the financial consequences. This tells you the worst-case scenario if you can’t reach an agreement. |

| Make Good Clause | This requires you to return the property to its original condition at the end of the lease. This still applies in an early exit. | Start budgeting for these costs now. They can be significant and are often a point of negotiation with the landlord. |

Reviewing these sections won’t just make you feel more in control—it gives you the knowledge you need to start a productive conversation with your landlord and, if necessary, your lawyer.

Know Where You Stand: Your Legal Rights and Obligations

Before you even think about breaking your commercial lease, you need to get crystal clear on your legal position. I’ve seen too many business owners act on assumptions, and it almost always ends in a costly, stressful dispute. Don’t make that mistake.

The world of commercial tenancy in Australia is a bit of a maze. Each state and territory has its own specific legislation that governs what landlords and tenants must do. For instance, in Western Australia, you’ve got the Commercial Tenancy (Retail Shops) Agreements Act 1985 for retail spaces, but other commercial properties might fall under different rules. Your rights aren’t just what’s written in your lease agreement; they’re also shaped by these laws. This is your starting point.

Finding a Legitimate Way Out

So, can you legally terminate the lease early? Maybe. It usually hinges on whether your landlord has dropped the ball on their responsibilities in a major way. We’re not talking about small annoyances here, but significant breaches that hit the very core of your agreement.

A classic example is the landlord’s failure to maintain the property. If a constantly leaking roof is destroying your stock, or the air conditioning is shot, making the space unusable for staff and customers—and you’ve told the landlord, but they’ve done nothing—you could have a solid case for termination.

Another powerful justification is a breach of an essential term in the lease. Think of an essential term as a deal-breaker condition; if it hadn’t been in the contract, you never would have signed. A common one is an exclusivity clause. Imagine you were promised the sole right to sell coffee in a small shopping centre, but then the landlord leases a kiosk to a competitor right opposite you. That’s a clear violation.

The key legal hurdle you’ll need to clear is proving ‘material prejudice’. This means showing that the landlord’s failure has caused your business significant harm. A substantial loss of income or major disruption to your operations would count. Simply being inconvenienced won’t cut it.

Your Side of the Bargain

Knowing your rights is only half the picture. You also have rock-solid responsibilities you can’t ignore, even if you’re planning to leave. Trying to sidestep these will expose your business to serious financial pain, no matter how justified you feel.

First up are the notice periods. Your lease document will state exactly how much written notice you need to give. Get this wrong, and you could invalidate your entire attempt to break the lease from the get-go.

Then there’s the often-dreaded ‘make good’ clause. This one trips up a lot of tenants.

- What it is: A contractual obligation to return the premises to the exact condition it was in when you first moved in.

- What it involves: This isn’t just a quick tidy-up. It can mean pulling out all your custom fit-outs, partitions, and signage, repainting walls to the original colour, and repairing any wear and tear.

- What it costs: The ‘make good’ bill can be a shock, often running into tens of thousands of dollars. It’s a significant expense that many businesses forget to budget for.

When you’re weighing up the costs of breaking a lease, always factor in your ‘make good’ obligations. A firm grasp of what you’re entitled to and what’s required of you is the only way to approach this strategically and shield your business from avoidable financial damage.

How to Negotiate an Early Exit with Your Landlord

Let’s be clear: getting out of a commercial lease early is rarely about finding a magic legal loophole. It almost always comes down to having a smart, strategic conversation with your landlord. The goal isn’t to start a fight, but to turn a tough situation into a problem you can solve together.

Think of it from their perspective. Your landlord is running a business, and their primary concerns are vacancy rates, the cost of re-letting the space, and maintaining a steady income stream. If you can frame your early exit as a solution that addresses these concerns, you’re on the right track.

Preparing Your Case for Negotiation

Before you even think about picking up the phone, you need to do your homework. Walking in and saying, “I need to leave,” is a non-starter. You have to build a professional case that explains why you need to exit and, more importantly, how you’ll make it as smooth as possible for them.

Get your documents in order to back up your story. This isn’t about oversharing, it’s about being transparent.

- Financials: If your business is struggling, be ready to show it. Profit and loss statements or cash flow forecasts can prove that staying is simply not viable. It shows this isn’t a whim.

- Business Plans: Moving because you’re expanding or need a different kind of space? Have the details on hand. A new, signed lease or a solid business plan shows this is a calculated strategic move.

- Market Data: Do a quick search for current vacancy rates and asking rents for similar commercial properties nearby. If the market is hot, you can make a strong case that they’ll find a new tenant quickly—maybe even at a higher rent.

This preparation shows you respect the landlord and the situation. You’re not just dropping a problem in their lap; you’re presenting a business reality.

Framing the Conversation for Success

Timing and tone are critical. Don’t ambush your landlord with a surprise call. Request a proper meeting to discuss the lease, which allows them to prepare as well. When you do sit down, your approach should be collaborative, not confrontational.

Kick off the conversation by acknowledging your obligations under the existing lease. It’s a simple sign of good faith that goes a long way. Then, calmly explain your situation, using the evidence you’ve gathered.

The best negotiations I’ve seen are when the tenant presents solutions, not just problems. A landlord’s number one fear is an empty property bleeding cash. If you can show them how to avoid that, they’re suddenly much more willing to listen.

Shift the focus from “I need to leave” to “how can we make this work for both of us?” This is your chance to table some creative, win-win alternatives.

Presenting Win-Win Alternatives

A savvy negotiation is all about offering options that reduce the landlord’s financial and administrative burden. By coming to the table with solutions, you prove you’re serious about finding a fair outcome. This proactive approach can save you a fortune in legal fees and keep your business reputation intact.

Consider putting a formal written proposal together with one or more of these options:

- Find a Replacement Tenant (Lease Assignment): This is often the most attractive option for a landlord. Offer to do the hard work of marketing the space, vetting potential tenants, and presenting a qualified candidate to take over your lease. The landlord gets a new, paying tenant with minimal downtime. It’s a huge win for them.

- Negotiate a “Surrender Fee”: Offer a one-off lump sum payment to terminate the agreement. This buyout, often equal to 2-6 months’ rent, gives the landlord a cash buffer to cover their costs while they find someone new. It gives you a clean, final break.

- Offer a Rent Subsidy: What if you find a great new tenant, but they can only afford slightly less rent than you were paying? Offer to cover the difference for a set period, say 6 or 12 months. The landlord’s income doesn’t drop, and you get to walk away.

By approaching this as a business partner looking for a practical solution, you completely change the dynamic. You’re no longer just a tenant breaking a contract; you’re helping them solve a potential problem. That kind of strategic communication is your best tool for securing an early, amicable, and cost-effective exit.

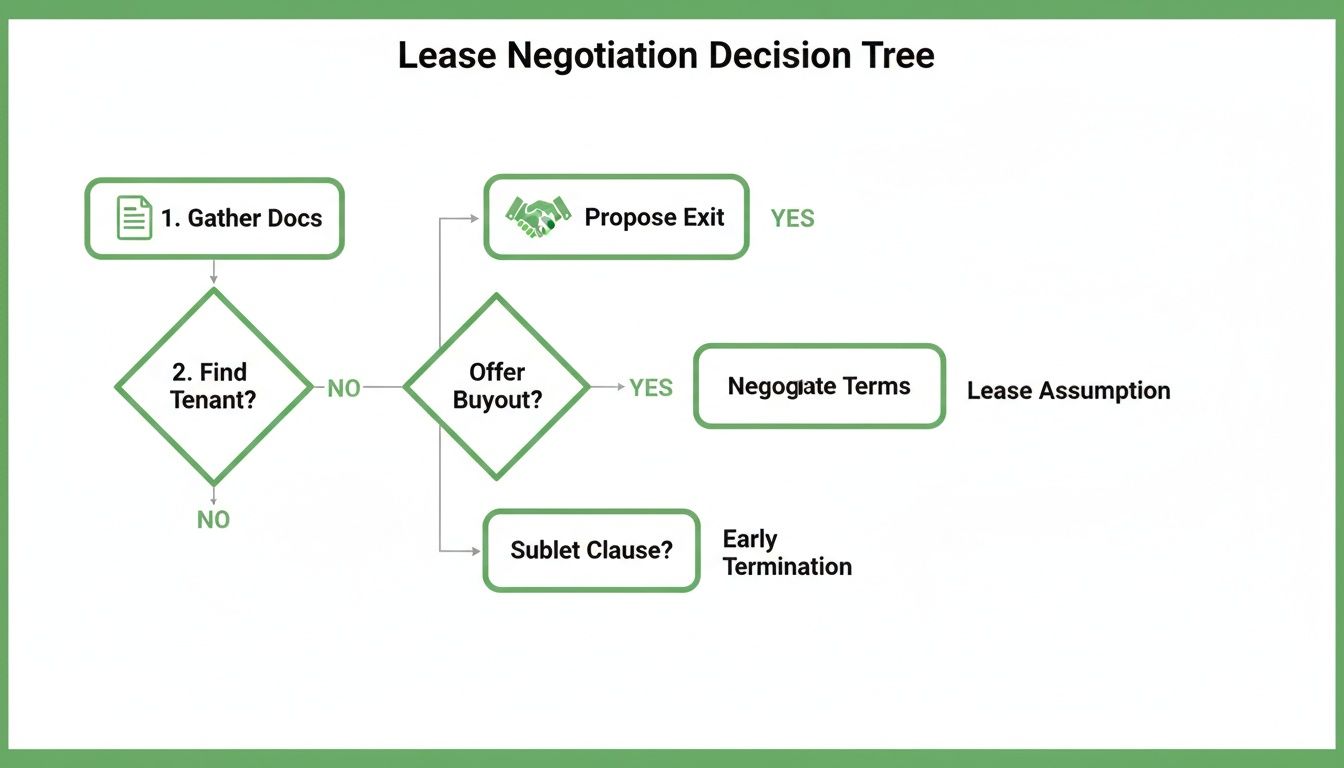

Making the Right Call: Your Lease Exit Options

So, you’ve decided you need to get out of your commercial lease. That’s the first step, but the next one is crucial: how are you going to do it? There’s no one-size-fits-all answer here. Each path comes with its own set of risks, costs, and ongoing headaches. Your final decision will really depend on your specific situation, how good your relationship is with the landlord, and what the local property market is doing right now.

Let’s walk through the three main ways you can tackle this: subleasing, assigning the lease, or negotiating a direct surrender. Getting your head around the fine print of each is the key to making a smart call for your business.

This whole process, from digging out your original lease documents to actually pitching an exit plan to your landlord, can feel a bit overwhelming. It helps to visualise it.

As you can see, the game changes dramatically depending on whether you can find someone to take your place. That’s often the biggest factor influencing your bargaining power.

Option 1: Subleasing Your Commercial Space

Subleasing is usually the first thing people think of when they need flexibility but aren’t looking for a permanent exit. Essentially, you find another business to move in and pay you rent. The catch? You’re still the one on the hook with the landlord.

This means you become a landlord yourself, which comes with its own set of responsibilities. If your subtenant doesn’t pay up or damages the property, that’s your problem. The landlord will be coming after you for the full rent and any repair costs.

A sublease makes sense if you’re facing a temporary dip in business or need to downsize for a year or two, but you think you might want the space back before your original lease is up. It keeps your options open.

Option 2: Assigning Your Commercial Lease

A lease assignment is a much cleaner break. With this approach, you find a new tenant who agrees to take over the rest of your lease term entirely. This new tenant, the “assignee,” effectively steps into your shoes and has a direct relationship with the landlord.

For most people wanting out, this is the gold standard. Once the landlord approves the assignment, you’re usually free and clear of any future obligations. Some landlords might ask you to guarantee the new tenant for a short period, but it’s a far more complete exit.

A lease assignment is typically the most desirable outcome for a tenant seeking a complete exit. It offers a clean slate, transferring both the rights and the responsibilities of the lease to a new party, effectively ending your relationship with the property.

Of course, finding that perfect replacement tenant is up to you. The landlord has to approve them and can rightfully reject anyone they don’t think is financially stable. They can’t just say no for no reason, but they will definitely do their due diligence.

Option 3: Negotiating a Surrender Agreement

The third route is to go straight to your landlord and negotiate a “lease surrender.” This is basically a buyout. You offer a lump sum payment—a surrender fee—and in return, the landlord agrees to tear up the lease and release you from all your obligations.

This is the most direct way to get a clean break without the hassle of finding a replacement tenant. The cost can vary wildly and really comes down to the market. If vacancy rates are low and they can re-lease the space tomorrow, they might ask for a hefty fee. But if the market is slow, they might be willing to take a smaller payment to avoid having a guaranteed empty property on their hands.

Market conditions across Australia really drive these negotiations. In Sydney, for example, the office vacancy rate recently fell to 11.6%, which means landlords there are in a strong position and less likely to cut you a deal. Over in Melbourne, however, the vacancy rate has shot up to 19.6%, giving tenants a lot more room to negotiate a favourable surrender.

Local nuances matter, too. In Perth, where industrial rents have been pretty flat, a landlord might be happy to waive any break fees if you can present them with a solid replacement tenant. If you’re planning a move within the city, it’s wise to get expert advice on https://emmanueltransport.net.au/insights-on-choosing-commercial-moving-services-in-perth/ to manage the logistics smoothly.

In a worst-case scenario where the business is insolvent, you’ll need to understand the broader consequences of bankruptcy and how that impacts your lease obligations.

Comparison of Lease Exit Strategies

To help you weigh your options, let’s put these three strategies side-by-side. Each has clear trade-offs between cost, effort, and how much liability you’re left with.

| Strategy | Your Ongoing Liability | Best For… | Typical Cost |

|---|---|---|---|

| Subleasing | High. You remain fully responsible for rent and property condition. | Temporary downsizing or short-term cash flow needs when you might return. | Minimal upfront cost, but high potential for future costs if the subtenant defaults. |

| Assignment | Low to None. Generally released from all obligations once approved. | A permanent, clean exit from the lease and the property. | Your time and marketing costs to find a replacement. Potentially some legal fees. |

| Surrender | None. The lease is terminated completely. | A guaranteed, immediate exit when you can’t find a replacement tenant. | A negotiated lump-sum fee, often equivalent to 3-6 months’ rent (or more). |

Ultimately, there’s no magic bullet. A sublease offers flexibility at the cost of risk, an assignment provides a clean break if you can do the legwork, and a surrender offers certainty for a price. Your choice will shape exactly how you break your commercial lease.

Calculating the True Cost of a Lease Break

Let’s get straight to the point: ending a commercial lease early will cost you. Before you even think about starting a conversation with your landlord, you need a crystal-clear understanding of the total financial hit. I’ve seen too many businesses turn a smart strategic exit into a financial nightmare simply because they miscalculated the costs.

The most obvious expense is the early termination penalty. This isn’t some fixed figure; it’s a moving target that will be heavily influenced by your lease agreement and what’s happening in the current property market. Essentially, you’re compensating the landlord for the risk and hassle of finding a new tenant.

Unpacking the Penalty Fees

When you’re trying to figure out the real cost of breaking a lease, you have to account for any potential fines and penalties baked into your agreement. These can show up in a few different forms, and it pays to budget for the most likely outcomes.

Here’s what you’re probably looking at:

- Remaining Rent Liability: In a worst-case scenario, the landlord could legally chase you for every dollar of rent left on your lease. This is the starting point for any negotiation.

- A Percentage Buyout: More often, you’ll negotiate a surrender fee. This is usually a lump sum equal to 50-100% of the remaining rent, giving the landlord a cash buffer while they search for a replacement.

- Covering Re-letting Costs: It’s common to be on the hook for the landlord’s costs to find someone new. This means paying for things like advertising, agent commissions, and the legal fees for drawing up a new lease.

Right now, in Australia’s industrial property market, a strong 86% rent retention rate gives landlords a lot of power. With post-pandemic rent collection sitting at 99%, owners are financially secure and have little incentive to be flexible. This means they can—and often will—enforce tough penalties.

The Hidden Costs of Making Good

Beyond the direct penalties, the “make good” clause is the hidden expense that catches everyone out. This is your contractual duty to return the property to its original state, and the costs can be eye-watering.

This is far more than just a quick clean. Your ‘make good’ obligations can involve some serious demolition and restoration work.

Don’t treat the ‘make good’ budget as an afterthought. I’ve seen these costs for a mid-sized office in Western Australia easily top $20,000. Getting a detailed quote from a fit-out contractor early is non-negotiable for a realistic financial picture.

Typical ‘make good’ jobs include:

- Removing Fit-outs: Every wall, custom cabinet, workstation, and light fitting you installed has to go.

- Floor and Ceiling Restoration: This means patching holes, replacing damaged carpet tiles, and putting the ceiling grid back to how it was.

- Repainting: You’ll almost certainly have to repaint the entire space in the original base colour.

- Service Decommissioning: Any special data cabling, security alarms, or extra plumbing you added will need to be professionally removed.

These are not DIY tasks; they require professional contractors. When you add the cost of physically moving everything, you can see how quickly it all adds up. To get a better handle on this, our guide on preparing for office furniture relocation in Perth breaks down what’s involved in the moving-out process.

By carefully calculating both the direct penalties and these often-overlooked ‘make good’ costs, you build a realistic budget. It allows you to properly weigh the cost of leaving against the pain of staying, ensuring your final decision is a smart one for your business.

Common Questions About Breaking a Commercial Lease

Deciding to break a commercial lease is a huge business decision, and it’s completely normal for your head to be swimming with questions. Getting straight answers is the only way to move forward confidently and sidestep any expensive pitfalls.

We’ll tackle some of the most common worries and “what-if” scenarios business owners face when they need to get out of a lease early.

What Happens If I Just Walk Away from My Lease?

It’s a tempting thought, especially when you’re under pressure, but I can’t stress this enough: just abandoning the property is the riskiest move you can make. Stopping rent payments and walking away is a clear breach of your lease, and the fallout can be severe.

Your landlord won’t just let it go; they’ll almost certainly take legal action. This means you could be sued for every dollar of rent remaining on the lease term, plus all the costs they rack up in the process, like their legal fees and the expenses of marketing the property to find a new tenant.

Simply walking away from a lease is a surefire way to wreck your business’s credit rating and professional reputation. It can make it incredibly difficult to get another commercial lease—or even business financing—down the track.

Ultimately, you surrender all control over the financial outcome. It almost always ends up being a much more expensive and damaging path than negotiating a proper exit strategy.

Can a Landlord Refuse My Request to Assign the Lease?

Yes, they can, but their refusal usually has to be reasonable. Your lease will definitely have a clause saying you need the landlord’s consent to assign it to someone else. The good news is that commercial tenancy laws across Australia generally imply that this consent can’t be withheld unreasonably.

So, what counts as “reasonable”?

- Financial Standing: A landlord can absolutely reject a potential new tenant if their financials look shaky. If they have a poor credit history or an unproven business model, the landlord has every right to say no. They need to be confident the rent will be paid.

- Proposed Use: If your proposed replacement plans to use the property for something completely different that violates the usage terms (think a quiet office being turned into a noisy gym), that’s a valid reason for refusal.

- Reputation: The landlord can also refuse a business with a bad reputation that might devalue the property or cause problems for other tenants.

What they can’t do is refuse just because they don’t personally like the new tenant or as a tactic to try and squeeze a bigger buyout fee from you.

How Does the Current Property Market Affect My Negotiations?

The local property market is probably the single biggest factor influencing your leverage. It all comes down to how much risk your landlord is taking on if you leave.

In a hot “landlord’s market,” where vacancy rates are low and businesses are lining up for space, your landlord has the upper hand. They know they can probably find a new tenant in no time, maybe even at a higher rent. In this situation, they have very little incentive to negotiate a smaller surrender fee.

But in a soft “tenant’s market,” with high vacancy rates and properties sitting empty, the power dynamic flips. A landlord’s biggest fear is a vacant property with no income. This makes them far more willing to come to the table, whether that means accepting a replacement tenant you’ve found or agreeing to a more reasonable exit fee.

Quick Answers to Your Questions

Getting your head around the specifics can be tricky, so here are some rapid-fire answers to the most pressing questions.

| Question | Answer |

|---|---|

| What happens if I just walk away from my lease? | You’ll be in breach of contract. Expect legal action to recover all remaining rent, legal fees, and other costs. This will severely damage your business credit and reputation. |

| Can the landlord refuse my request to assign the lease? | Yes, but their refusal must be reasonable. They can reject a new tenant based on poor financials or an unsuitable business use, but not for personal dislike or to gain leverage. |

| How does the current property market affect my negotiations? | In a landlord’s market (low vacancy), you have less power. In a tenant’s market (high vacancy), landlords are more motivated to negotiate to avoid an empty property. |

Remember, every situation is unique, and getting advice tailored to your specific circumstances is always the best course of action.

Navigating a commercial relocation involves more than just lease negotiations. For a seamless move that minimises business downtime, trust the experts at Emmanuel Transport. Our professional team handles every detail of your office move across Perth, from packing and logistics to reassembly, ensuring your business is back up and running as quickly as possible. Contact us for a transparent, no-obligation quote today.