Relocation insurance is coverage that protects your belongings against loss, damage, or theft while they are being transported from one location to another. The industry term for this protection is “moving insurance” or “transit insurance,” though relocation insurance is the phrase most people search for. Homeowner and renter policies typically do not cover possessions in transit, which means the gap between your front door and your new address is often completely unprotected. Whether you are moving a household across Perth or relocating a business across the country, understanding what relocation insurance covers before moving day is the difference between a manageable setback and a serious financial loss.

What is relocation insurance and what types of coverage exist?

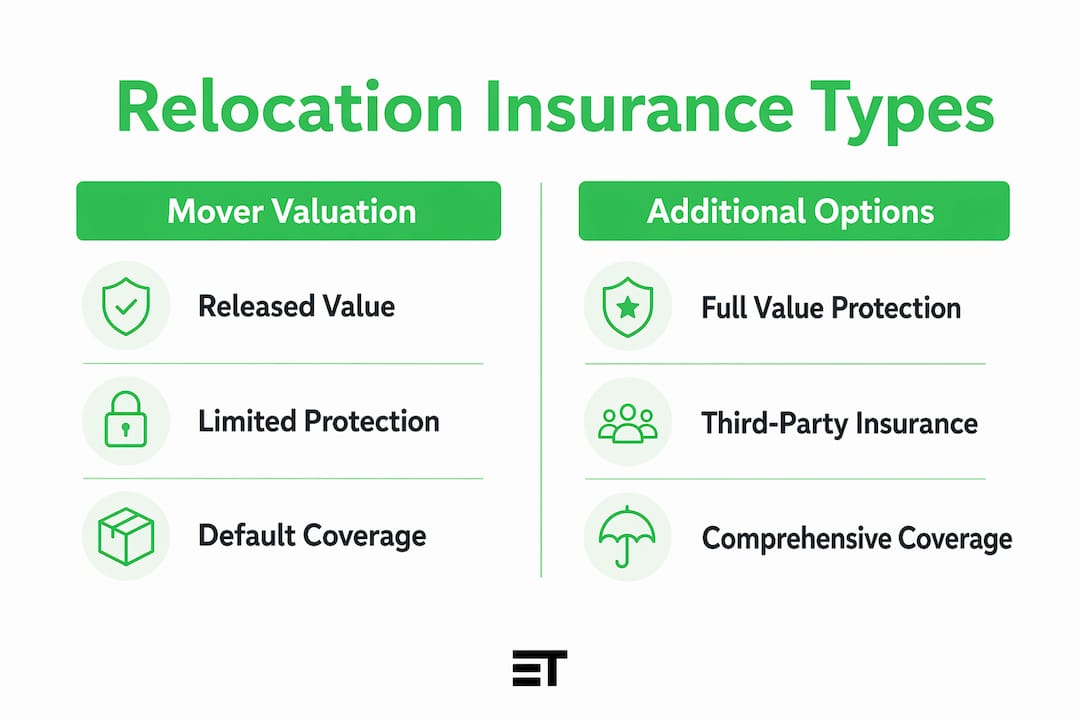

Relocation insurance reimburses you for loss or damage of goods while they are in a mover’s custody, including theft and fire depending on the policy terms. Three main coverage types exist, and each operates very differently. Knowing which one applies to your move determines how much protection you actually have.

Released value protection

Released value protection is the default coverage most removalists include at no extra charge. The catch is that it pays based on weight, not value. In Australia, this type of coverage typically pays a fixed rate per kilogram per item. The American equivalent, regulated by the FMCSA, pays $0.60 per pound per article, which illustrates the problem clearly. A one-kilogram laptop worth $2,000 could receive a payout of less than a dollar under this structure. Released value protection is better understood as a liability limit than genuine insurance.

Full value protection

Full value protection, sometimes called full replacement value protection, is an upgrade that must be purchased separately. Under this coverage, the mover is liable to repair, replace, or pay cash based on the current market value of a lost or damaged item. If your television is broken during the move, the mover must either fix it, replace it with a comparable model, or pay you its current market value. This is a meaningful improvement over released value protection, though the specific terms on how replacement value is calculated vary between providers.

Third-party moving insurance

Third-party moving insurance is a separate policy purchased from an insurer rather than the removalist. These policies provide broader coverage than mover valuation, typically operating on an all-risk basis unless specific exclusions apply. Named-perils policies, by contrast, only pay out for causes of loss that are explicitly listed in the policy document. All-risk coverage is the stronger option because the insurer must prove an exclusion applies to deny a claim, rather than you having to prove your loss falls within a covered category.

Pro Tip: When comparing policies, focus on how claims are reimbursed rather than the coverage name. Repair, replacement with a similar item, and cash settlement at current market value are three very different outcomes for the same damaged sofa.

The table below compares the three main coverage types at a glance.

| Coverage type | Cost | Basis of payout | Best suited for |

|---|---|---|---|

| Released value protection | Usually free | Weight per item | Low-value goods only |

| Full value protection | Paid upgrade | Current market value | Most household moves |

| Third-party all-risk insurance | 1% to 5% of declared value | All causes unless excluded | High-value or complex moves |

- Released value protection is the minimum and rarely adequate for modern households.

- Full value protection is the most common upgrade offered by removalists.

- Third-party insurance is the only option that operates as a true insurance policy.

- All-risk policies shift the burden of proof to the insurer, not the policyholder.

How does relocation insurance work in practice?

Understanding how relocation insurance works means knowing what happens after something goes wrong, not just what the policy promises before the move. The claims process, documentation requirements, and common exclusions all shape whether you receive a fair payout.

- Document everything before the move. Photograph each item, note existing damage, and create a detailed inventory list. Keeping records before and after the move speeds the claims process and improves your chances of full recovery. Without this documentation, insurers and removalists have grounds to dispute the extent of any damage.

- Understand the difference between valuation coverage and insurance. Valuation coverage is a carrier’s liability limit, not an insurance policy. This distinction matters legally and practically. A removalist’s valuation coverage is governed by the contract you sign with them, while a third-party insurance policy is regulated by Australian financial services law.

- Lodge claims with both parties simultaneously when applicable. If you hold both mover valuation coverage and a third-party policy, simultaneous documentation submission to both the mover and the insurer is required. Delaying one claim while waiting on the other can void your entitlements.

- Know the common exclusions. Owner-packed boxes are a frequent exclusion. If you pack your own cartons and something inside breaks, most policies will not pay out unless there is external damage to the box itself. Mechanical or electrical derangement without visible external damage is another common exclusion.

- Declare high-value items separately. Art, jewellery, antiques, and collectibles often exceed standard valuation limits and require individual declarations with supporting appraisals. Scheduling these items individually leads to faster and more accurate reimbursement outcomes.

Pro Tip: Get a written appraisal for any item worth more than $1,000 before moving day. Declaring high-value items individually with appraisals produces faster and more accurate insurance payouts than relying on general declarations.

For items like fine art or jewellery that exceed standard policy limits, a separate inland marine insurance policy may be the only way to achieve full coverage. This is a specialist product available through insurance brokers and is worth investigating well before your move date.

Who needs relocation insurance and what are the benefits?

The benefits of relocation insurance extend beyond simple financial reimbursement. Every move carries physical risk to your goods, and the level of risk scales with the value of what you own, the distance of the move, and the complexity of the logistics involved.

Consider what is actually at stake during a typical household move. Furniture is carried through narrow doorways, loaded onto trucks, transported over roads, and unloaded again. Even with experienced removalists and proper furniture protection, accidents happen. A single dropped item or a vehicle accident can result in thousands of dollars in losses. Relocation insurance converts that unpredictable financial risk into a known, manageable cost.

The following situations make relocation insurance particularly worth considering:

- Moves involving high-value goods. Electronics, artwork, musical instruments, and antique furniture all carry replacement costs that far exceed what released value protection would pay.

- Interstate or international moves. Longer transit distances mean more handling, more time on the road, and greater exposure to risk. Interstate moving costs already represent a significant investment, and protecting the goods being transported is a logical extension of that investment.

- Business relocations. Office equipment, servers, and specialised machinery are expensive to replace and critical to operations. A business that loses key equipment during a move faces both replacement costs and lost productivity.

- Moves with fragile or irreplaceable items. Family heirlooms, original artwork, and custom furniture cannot be replaced at any price. Insurance at least provides financial compensation when physical replacement is impossible.

- Renters and homeowners without transit coverage. Existing policies rarely cover goods in transit, which means most people are uninsured during the move itself without realising it.

Many customers supplement mover valuation with third-party insurance for high-value shipments, and this combined approach provides the most complete protection available. The mover’s valuation coverage handles claims within its scope, while the third-party policy fills the gaps.

What factors influence the cost of relocation insurance?

The cost of relocation insurance is directly tied to the declared value of your shipment, the type of coverage you choose, and the specifics of your move. Relocation insurance typically costs between 1% and 5% of the declared shipment value. That means a $50,000 household shipment could cost between $500 and $2,500 to insure fully, depending on the policy.

| Factor | Effect on cost | Notes |

|---|---|---|

| Coverage type | Major | All-risk costs more than named-perils |

| Declared shipment value | Direct | Higher value equals higher premium |

| Deductible amount | Inverse | Higher deductible reduces premium |

| Move distance | Moderate | Interstate and international cost more |

| Item specifics | Variable | High-value items may require separate declarations |

Released value protection is free because it offers minimal protection. Full value protection and third-party all-risk policies carry a cost, but that cost is proportional to the protection they provide. Choosing a higher deductible is one straightforward way to reduce your premium while maintaining coverage for catastrophic losses.

Declared value accuracy matters more than most people realise. Undervaluing your shipment to reduce the premium is a false economy. If you declare $20,000 worth of goods but your actual losses are $40,000, your payout is capped at the declared amount. Take the time to create an accurate inventory with realistic replacement values before you request a quote.

Pro Tip: Use a moving cost comparison to understand the full picture of your move budget, then allocate a realistic amount for insurance rather than treating it as an afterthought.

Local moves within Perth generally attract lower premiums than interstate moves because the transit time and handling exposure are reduced. International moves carry the highest premiums due to customs handling, sea or air freight risks, and the complexity of cross-border claims. If you are moving interstate, factor insurance into your budget from the start rather than adding it at the last minute when you may have fewer options.

Key takeaways

Relocation insurance is the only reliable way to protect your belongings financially during a move, and choosing the right coverage type determines whether a payout actually reflects your loss.

| Point | Details |

|---|---|

| Three coverage types exist | Released value, full value protection, and third-party insurance each offer different levels of payout and protection. |

| Existing home policies have gaps | Homeowner and renter insurance typically does not cover goods in transit, leaving most people unprotected during a move. |

| Documentation drives claims success | Inventories, photographs, and appraisals before the move are the single biggest factor in a successful insurance claim. |

| Cost scales with declared value | Insurance typically costs 1% to 5% of declared shipment value, making accurate valuation critical to adequate coverage. |

| High-value items need separate cover | Art, jewellery, and antiques often require individual declarations or inland marine policies beyond standard moving insurance. |

What I have learned from years of moving Perth households and businesses

The most common mistake I see is people confusing the removalist’s valuation coverage with actual insurance. They sign the contract, see the word “coverage,” and assume they are protected. They are not, at least not in any meaningful sense. Released value protection is a contractual liability limit, not a financial safety net. When a $3,000 television gets damaged and the payout is less than $5, the disappointment is real and entirely avoidable.

The second mistake is packing your own boxes and assuming the policy still applies. Most policies exclude owner-packed cartons from damage claims unless there is visible external damage to the box. If you are going to pack your own items, photograph the contents before sealing each box. It takes ten minutes and it is the only evidence you will have if something inside is broken.

For businesses, the stakes are higher and the preparation needs to be more thorough. A server rack or a piece of specialist equipment is not just expensive to replace. It represents downtime, lost data risk, and operational disruption. I would always recommend a separate inland marine policy for business equipment rather than relying on a standard moving insurance product.

The advice I give everyone, whether they are moving a studio apartment or a full commercial office, is to treat the insurance decision with the same seriousness as the removalist selection. Read the exclusions before you sign. Declare your high-value items individually. And never undervalue your shipment to save a few dollars on the premium. The premium is the smallest cost in a move gone wrong.

— Emmanuel

Move with confidence: how Emmanuel Transport can help

Emmanuel Transport provides residential and commercial removalist services across Perth and surrounding suburbs, with a focus on careful handling and transparent pricing. When you book with Emmanuel Transport, you get experienced staff who understand the importance of protecting your goods from the moment they leave your door. Our team can guide you through protection options for your move and help you understand what coverage makes sense for your specific situation. Whether you are moving a family home or relocating a business, explore our Perth residential removals service and request a free quote today.

FAQ

What does relocation insurance cover?

Relocation insurance covers loss, damage, and theft of your belongings while they are in transit during a move. Depending on the policy, coverage may include fire, accidents, and handling damage, with exclusions typically applying to owner-packed boxes and pre-existing damage.

Is relocation insurance the same as mover valuation coverage?

No. Valuation coverage is a contractual liability limit set by the removalist, while relocation insurance is a separate financial product regulated as insurance. Third-party moving insurance policies provide broader protection and operate under different legal frameworks.

How much does relocation insurance cost?

Relocation insurance typically costs between 1% and 5% of the declared shipment value, depending on coverage type, deductible, and move distance. Released value protection is usually included at no charge but offers minimal payout based on weight rather than item value.

Does my home insurance cover goods during a move?

Most homeowner and renter insurance policies do not cover possessions in transit. You need either mover valuation coverage or a separate transit insurance policy to protect your goods during the move itself.

Do I need relocation insurance for a local move within Perth?

Yes, particularly if you own high-value electronics, furniture, or fragile items. Local moves carry lower premiums than interstate moves, making coverage relatively affordable relative to the protection it provides.